Retrieve this SKU-level transaction data programmatically via the Knot API

Knot’s transaction data is unique, here’s why…

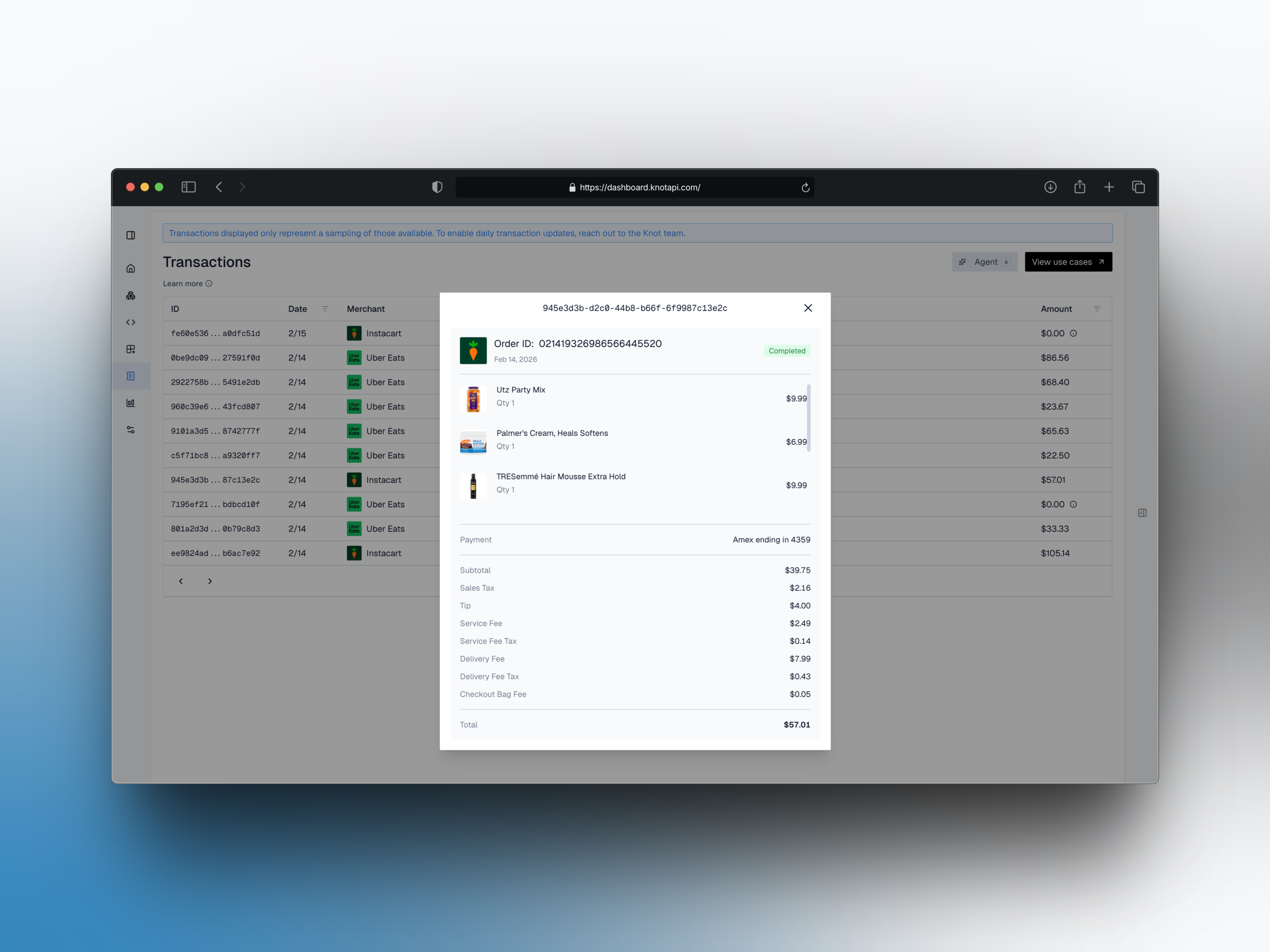

Each transaction includes all of the following information:- Exact products (SKUs) that were included in the purchase, including their brand name, price, and quantity. This qualifies the transaction data as Level 3 (L3) and provides extreme granularity into a user’s spending habits.

- Payment method(s) used in the transaction (e.g. card, BNPL, Apple Pay, cash, etc.), whether single-tender or split-tender, providing share-of-wallet and competitive insights.

- Receipt-level price information, including the subtotal, list of adjustments (e.g tax, tip, fees), and total.

- Status of the order (e.g. shipped, delivered, picked up, etc.), unlocking fulfillment lifecycle visibility.

- Much more…

- Both historical and future transactions.

- Both online and in-store transactions.

- Transactions made on all payment methods, including competitive payment methods to the card(s) you may issue (e.g. other cards, digital wallets, BNPL providers, cash, etc.).

Use cases

AI-assistant

If you have plans to integrate an AI-financial assistant into your product (or already have this concept), such a tool becomes significantly more powerful with access to a user’s SKU-level transaction data. The assistant could monitor a user’s purchasing behavior, unlocking any of the following “sub-use cases”:- Smart budgeting suggestions, such as “You’re buying snacks three times a week — switching to bulk orders on Amazon could save you

$25/month.” - Anomaly detection, such as “You usually spend

$60–$80on groceries, but this week’s Walmart order was$150. Was that intentional?” - Receipt-level contextual responses, such as being able to answer “Show me what I bought at Target last Tuesday”.

- Cashback recommendations by identifying existing brands purchased and recommending for example “You could earn 5% back at this month on your La Croix purchase if you buy at Target.”

- Financial coaching, such as mentioning “You spent

$120on takeout this week — that’s 3× your usual average. Cooking twice at home could save$80/month.” - Cross-sell product recommendations, such as “I noticed you use Affirm frequently to pay for products at Walmart. Take a peek at our new XYZ credit product to lower your rate.”

- Personalized shopping assistance, such as offering the following: “You usually buy school snacks from Walmart. Want me to check if Target has them cheaper this week?”

- Meal planning by offering relevant recipes like “You bought pasta, sauce, and garlic bread today — want me to suggest three 20-minute dinner recipes using those ingredients?”

Disputes (for issuers)

First-party fraud deflection

By displaying the exact items purchased in a transaction, along with their fulfillment details, such as order status and delivery confirmation, you can dramatically reduce instances of first-party or “friendly” fraud, where users dispute charges they knowingly made. When customers see the exact product(s) they purchased in a transaction and that the purchase was delivered to their address, most reconsider filing a dispute. This visibility creates an implicit trust moment between the user and your institution, replacing confusion or doubt with clarity. In practice, showing a line-item breakdown (“LEGO City Set, Pokémon Booster Pack, and UNO Card Game — delivered on Nov 4, 2025”) serves as a natural deterrent: users instantly recognize the transaction as legitimate, saving your team time & money spent on unnecessary chargeback investigations.Competitive insights

Share of wallet

Each transaction includes the payment method(s) used for the purchase across all payment methods stored in the user’s merchant account (the full list found here). Therefore, for a given user or across your entire use base, you can determine the spend going towards competitive payment methods. This can give you a sense for how much spend you could be capturing onto your card, as well as the % of spending you’re already capturing across grocery, retail, and other discretionary spend.Cross-sell new products

For users purchasing with competitive payment methods to your own card or other payment products, you can determine that certain of your payment products may be desirable alternatives to those users. For example, you may identify users purchasing with BNPL products and choose to offer them access to your new credit card that offers better rates and more rewards.Rewards

Design a more tailored rewards program

Fundamentally, if you can understand the brands and even specific items or services that users purchase, then you can be more strategic about designing your rewards program. Through the identification of specific brand affinities across your user base, you can seek to develop more tailored merchant partnerships to provide more relevant reward offers to your users, even providing CPG-brand or item-level offers (as opposed to merchant-level).Brand & SKU-level reward offers

With SKU-level transaction data, you can create and offer CPG-brand and item-level reward offers to your users - cashback, points, discounts, or other incentives. Specifically, by monitoring exactly which brands a user purchases, you can offer rewards to that user on their brands-of-choice and different brand-specific offers to other users. This allows for a hyper-tailored rewards program. Additionally, you can easily determine that a user purchased a product from a specific brand (or even a particular product) and subsequently credit that user for their rewards. Examples:- “Earn 6x points on Under Armour socks at Target”

- “Earn 10% cash back on Spicy Cumin Hand-Ripped Noodles at Xian Famous Foods on DoorDash until 11/6/25”

EBT spending rewards

If a particular purchase is made with an EBT SNAP or other EBT balance, you will receive this information in each transaction. Therefore, you could offer rewards on EBT card spend for those frequently using government benefits to purchase groceries and other household staples.Savings

Price comparison

Transactions include the price of each product purchased in the transaction. This provides you with visibility into whether a particular user is purchasing cheap or expensive products and allows you to compare the price of those products to those of other users in order to recommend savings. For example, you may see a particular user purchasing a 12 pack of Waterloo seltzer at Target each week for$22, but you also notice other users purchasing the same item at Walmart for $12. So, you can recommend that the first user consider purchasing their 12 pack of Waterloo seltzer at Walmart instead to save them $10/week.

FSA/HSA reimbursement

Using the eligibility of each product in a transaction, you can determine whether a particular product is eligible to be retroactively reimbursed from an FSA/HSA account. If a product is eligible for reimbursement, automatically submit a reimbursement on the user’s behalf to save them money.Spending insights

Know what you bought

When you open your banking or fintech PFM app and look through your purchases, you may see a cleaned up name of the merchant for each purchase, at best. Therefore, you can determine that a particular$36.58 purchase was at DoorDash, but you still have no idea what you bought. This is the L3 transaction data gap. With transaction from Knot, you can simply display what a user purchases on each transaction. You may have a dedicated screen in your app for each transaction and now you list the exact items that were purchased in that transaction.

This functionality deeply enriches the usefulness of your app by giving users additional visibility into their purchases, particularly to ensure that they made those purchases, rather than a fraudulent actor. It’s peace of mind!

Hyper-granular budgeting

You can automatically categorize purchases into categories far more granular than those possible with transaction data from open banking platforms or networks. Instead of relying on MCC codes or categories derived from MCC codes (via transaction enrichment providers), identify transaction categories based on precisely what is included in a purchase. Even categorize a single purchase across multiple categories. For example, let’s say you see that a user made the following $114.68 purchase at Walmart:- 2 bags of Smartfood white cheddar popcorn

- 1 bag of nacho cheese doritos

- 3 family-size bags of Tostitos scoops

- 2 cases of la croix sparking water

- 2 packs of organic chicken breast

- 3 heads of lettuce

- 5 tomatoes, on the vine

- 1 bag of dry, basmatic rice